Global S&T Development Trend Analysis Platform of Resources and Environment

| From Banks to Capital Markets: Alternative Investment Funds as a Potential Pathway for Refinancing Clean Energy Debt in India | |

| Divjot Singh and Dhruba Purkayastha | |

| 2019-08 | |

| 出版年 | 2019 |

| 语种 | 英语 |

| 国家 | 美国 |

| 领域 | 气候变化 |

| 英文摘要 | Dr. Gireesh Shrimali, CPI’s former India Director and Senior Advisor is also an author. Clean energy must play a central role in achieving India’s green growth goals. The IFC estimates India will need $450 billion to finance its 2030 clean energy targets (IFC 2017). Assuming a typical 70-30 split of financing via debt vs equity, the debt funding requirements translate to $315 billion through 2030. While India’s clean energy sector continues to grow and attract significant investment, there can be serious challenges to the growth trajectory, if the capital deployed in existing projects is not recycled and if new sources of capital are not included to meet the increased future investment requirements (Pragathi and Veena, 2018). It is, therefore, imperative that operational renewable energy projects access capital markets to recycle capital and attract new investor classes. This study, produced by Climate Policy Initiative under the US-India Catalytic Solar Finance Program (USICSF), and as a knowledge partner with the Indian Renewable Energy Development Agency (IREDA), looks at various avenues for renewable energy to access capital markets. We show that shifting project debt to capital markets can be primarily achieved via two pathways:

These paths are common in economies with more developed capital markets, however, in India, barring a few sporadic transactions, both pathways are yet to take off in any substantive manner. We therefore suggest specific solutions that would help to address some of the main barriers in the medium and longer term. These include:

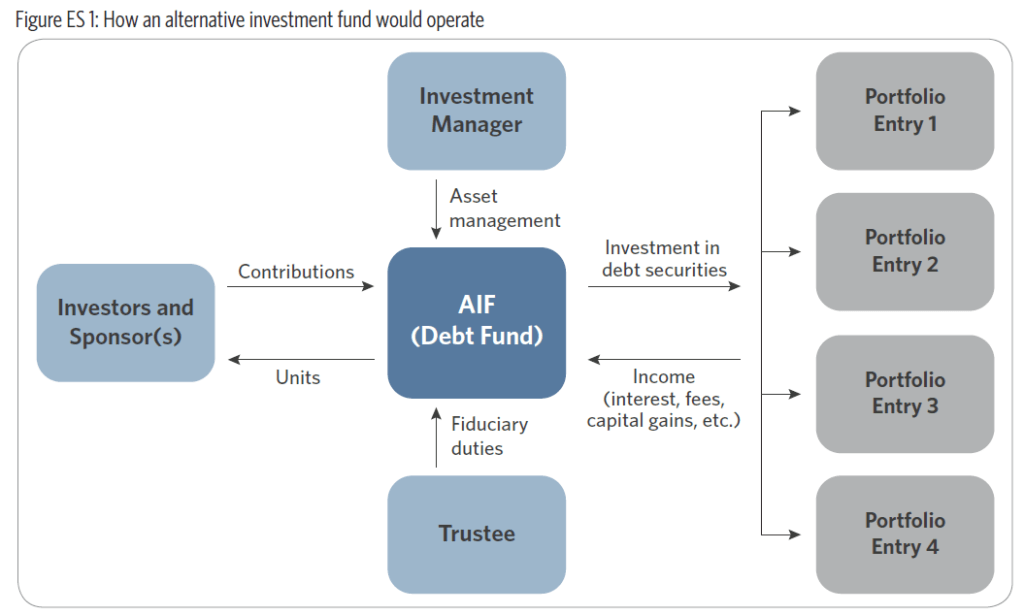

In addition, our research shows that Alternative Investment Funds (AIFs) offer the best near and medium-term path to expanding renewable energy access to capital markets while more structural issues are addressed. AIFs are essentially managed pools of money that can invest in a pre-specified mandate. As the name suggests, AIFs are alternatives and can deploy investment strategies that are beyond the purview of the more commonly deployed pathways such as mutual funds – e.g. investing in startups/unlisted companies, deploying leverage and complex trading strategies, etc. Through participation of institutional investors, an AIF allows investment in debt securities issued by renewable energy project developers, which are backed by cashflows from stable and operational projects. The proceeds from bond issuances can then be used to retire loans that the developers would have taken from banks/NBFCs. While AIFs may not fully address the structural issues prevalent in the Indian capital markets, they may partially resolve or help to circumvent some of these barriers, such as, by:

Further, AIFs appear to be the most flexible of similar instruments (e.g., INVITs and IDFs) and, therefore, are likely to be more successful in taking renewable projects to capital markets. This study recommends that potential sponsors work toward a next step of a demonstration AIF focused on renewable energy debt. Such a project – particularly if offered by a public agency like IREDA – could provide useful demonstration effects, and create track record to build investor confidence about the economic viability of clean energy projects, offering potential for further replication of this model.

|

| 英文关键词 | capital markets climate finance climate investment developing economies financial innovation financial institutions fiscal policy renewable energy renewable energy investment |

| URL | 查看原文 |

| 来源平台 | Climate Policy Initiative |

| 文献类型 | 科技报告 |

| 条目标识符 | http://119.78.100.173/C666/handle/2XK7JSWQ/242576 |

| 专题 | 气候变化 |

| 推荐引用方式 GB/T 7714 | Divjot Singh and Dhruba Purkayastha. From Banks to Capital Markets: Alternative Investment Funds as a Potential Pathway for Refinancing Clean Energy Debt in India,2019. |

| 条目包含的文件 | ||||||

| 文件名称/大小 | 文献类型 | 版本类型 | 开放类型 | 使用许可 | ||

| Alternative-Investme(538KB) | 科技报告 | 开放获取 | CC BY-NC-SA | 浏览 请求全文 | ||

除非特别说明,本系统中所有内容都受版权保护,并保留所有权利。

修改评论